Option skew represents out of the money bets on a crash.

Skew has only been 170 or greater 6 times and 4 of those times were last week

At the same time the SPX hit a record high week and the VIX traded at its lowest point since July.

It’s a conundrum: record skew and a collapsing VIX.

How to resolve the seeming disparity?

Money managers are being forced into performance chasing.

When it within 7 weeks of year-end. A little chasing can cause more chasing just as momentum begets more momentum.

At the same time they aren’t stupid and while they are putting client’s money at extreme risk they know how these parties end and are betting on the likelihood of a black swan event that would be a catalyst to unwind a slug of one-side bets.

Perpetuating the performance chasing is none other than the Fed and other Central Banks who have set the stage for what the vast majority of market participants anticipate will be a year of monetary easing.

Isn’t this deja vu all over again. Wasn’t this year supposed to deliver an array of rate cuts?

And if the Fed stands and delivers does the market call B.S. on it again and send yields higher?

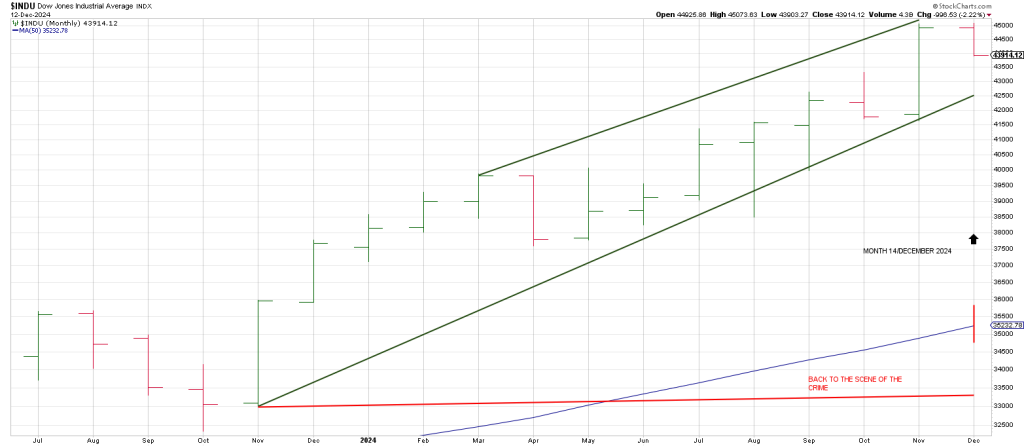

This parabolic party started in late October 2023.

December is the 14th month (7 X2) from low.

Interestingly, the blow-off in 1929 ended on the 14th month.

The 14th month from of the blow-off in 1929 was September.

The DJIA left Train Tracks.

October 1929 saw a collapse back to where the party started, kissing the 50 month moving average.

Theoretically, if this pattern plays out the SPX would revisit the 4100 region.

It’s intriguing that 410 (4100) vibrates (180 degrees opposition) October 29th which essentially is the low day in October 2023 where this momentous advance started.

The low close was October 27th, 2023. The next trading day was October 30th when the SPX gapped up followed by a series of Breakaway Gaps.

In sum there are several ‘correspondences’ to the euphoria that permeated the last run in 1929.

Earlier this month we showed a chart reflection the 3 spikes into the highest P/E ratio markets.

1929, 2000 and 2024.

From 1929 to the 2000 top is 71 years.

From the 2000 top to 2025 (a few weeks off) is 25 years.

The relationship between these periods ties to a major square-out in time.

Allow me to explain.

1.618 is the Golden Ratio, or Phi that appears in many natural and human-made forms.

It is often referred to as the Divine Proportion.

1.618 squared is 2.61.

If we divide the aforesaid 71 year period by the current 25 year period we get 2.8.

We’re in the Wheelhouse.

Two years from now in 2027 is precisely 2.6.

Theoretically, the market could hold up another 2 years using this relationship.

But the math could be pointing to a high to high to low cycle…with a low in 2027…two to three years after a presumed top in this vicinity.

2027 is a year ending in 7 which often mark panics or the start of panics:

1907, 1937, 1987, 2007, 2017 (an upside panic).

The SPX is up 24 points as I write this overnight. Ostensibly on the heels of AVGO earnings.

AVGO is up 26 points to 207 pre-market.

It closed November at 152.

Earning’s Lollapalooza continues…in both directions.

ADBE got hammered 75 points last night after results.

RH is ripping 68 points after backtesting its Breakout Pivot yesterday.

It is no small matter that the DJIA is on the longest losing streak since April.

We discussed the pattern of the DJIA, SPX, NAZ in 2000 in this space yesterday.

As well The Truth Teller, IWM, closed decisively below its 20 day moving average on Thursday.

The market is reminiscent of late 2007 when the writing was on the wall, but nothing mattered until January 2nd, 2008 when the plug was pulled.

Never underestimate the backing and filling required to forestall a big year of gains into the next year for tax purposes.