The SPX and QQQ gapped up to record highs for a second consecutive day on Monday.

Well-defined potential Megaphone Tops on both indices starting from September 22 morphed into breakouts from mini Cup and Handles.

The SPX is now just 150 points from our idealized 702 (7020) potential Time/Price square-out with the November 7 to November 13 time frame, a time period we have been focusing on for the last few months.

To recap, November 7 squares 43. The secular bull market began 43 years ago in 1982.

November 7 is conjunct/points to the year 2025.

November 13 is the crash low in 1929 for a possible mirror-image fold-back…low to high.

The 483 (4830) April 7, 2025 low is straight across and opposite November 13,

720 degrees in price up from 483 is 675 (6750). Another 90 degrees up for a possible Throw Over is 702 (7020).

At the 7000 region, there are a lot of possible Gann “7” Panic to consider:

1) 7000 SPX

2) November 7 is 7 months from the April 7 low.

3) We are 7 years from the November pivot that was followed by a crash into Xmas in 2018—SEVEN years ago.

We have a Breakaway Gap…Friday, a Continuation Gap…Monday.

Will today produce a 3rd gap that is a possible Exhaustion Gap?

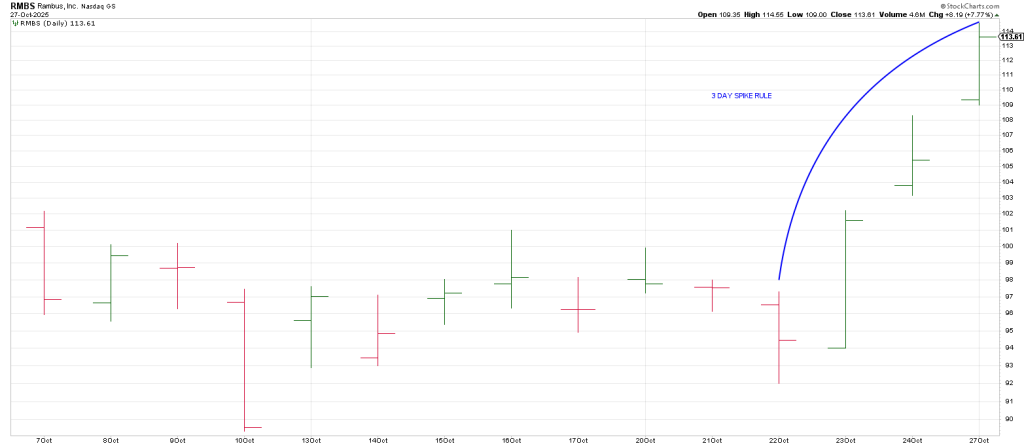

A 3 Day Spike Rule may play out.

RMBS is a good example. Reporting after Monday’s close following a 3 Day Spike, RMBS caved in 14 points.

For its part, the Q’s bottomed at 402.39 on April 7.

627/628 is 720 +180 degrees up from 402 for 900 degrees.

402 and 628 square-out with November 2/3.

As you recall there is what I call a Crash Cycle on November 4 hitting.

This does not time a crash…what it does is cap price and start the clock if one is going to appear.

This cycle occurred on September 7, 1929, 4 days after the top.

It occurred on May 14, 1987, squaring the top 90-100 days later.

It occurred on August 29, 2000 right at the Secondary Top.

It occurs on November 4, 2025.

Gann’s time keepers are Jupiter and Saturn. Their conjunctions occur around every 20 year.

Three conjunctions produces what Gann Called his Master Time Factor.

On August 23, 1929 Saturn (the bad guy) went direct. He exerted his influence.

On October 5, 1929, Jupiter (the good guy—expansion) went retrograde diminished influence.

A chart of the DJIA in 1929 shows a “normal” pullback into October 4th testing the 200 DMA which

Perpetuate a 5 day rally. When the DJIA broke the October 4 low, all hell broke loose.

What looked like a normal pullback to the 200 DMA which hadn’t been tested in a year reaped the whirlwind.

When the Jupiter Retro level of October 5 snapped, the crash was triggered.

In 1987 the market topped on August 25 and crashed on October 19.

On August 19, 1987 Saturn the bad guy went direct.

The same day Jupiter the good guy went retrograde, and expansionary power went with it.

Here in 2025 Jupiter goes retrograde on November 11, right into our time zone for a turning point.

Saturn goes direct on November 25.

The market is spiking into November just as it spiked into early September 1929 and late August 1987.

This week is a key week not just because of this potential time/price synergy but because 5 of the Mag 7’s report and we get the Fed.

While the background news remains broadly optimistic, a closer look beneath the surface reveals an increasing divergence between visible strength an underlying weakness— a pattern with clear echoes of prior market peaks.

Going into this week three developments have fueled the latest advance.

First the SPX close above its prior all-time high,

Second, the weekend’ China hoped for trade agreement prove more favorable than the worst case scenario feared earlier this month.

Third, the Fed’s expected rate cut has added to improve sentiment and short-covering creating momentum.

Yet the weight of evidence warrants caution that this spike is climatic.

NAZ downside volume this last week was the highest in history, indicating aggressive distribution.

This combination—policy optimism, surface-level strength, and deteriorating internals—ha appeared before at major turning point. In early 2000, late 2007 an again in late 2021, narrow leadership and record high indexes masked deep internal erosion. Each time, the apparent breakout proved to be the last gasp of a maturing bull cycle.

The bond market is already pricing in a 100% probability of a rate cut, meaning the expected easing is fully discounted.

Likewise while the China ‘deal’ injected a positive tone, it merely avoided further escalation, an outcome the market had already assumed.

In sum, much of what now sustains the bullish narrative has already been reflected in price, leaving little room for upside surprise.

Mag earnings could fuel the spike to 7000.

Meanwhile, internal breadth continues to weaken showing the poorest readings ever recorded at an SPX high.