On Wednesday the SPX gapped up but closed on session lows.

The Roadmap was correct but it was a pyrrhic victory—the ‘rollover’ was nothing to write home about.

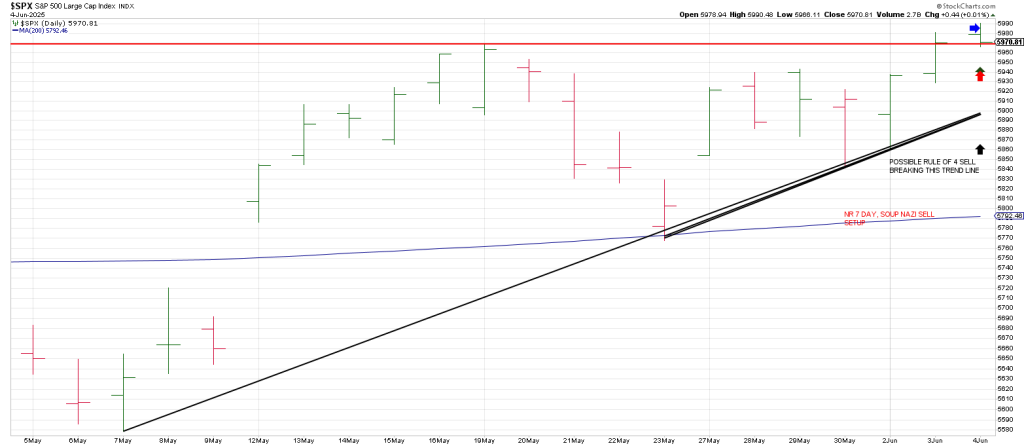

Be that as it may, the SPX left an NR 7 Day. This is the narrowest range in 7 days.

Such contractions in volatility are usually followed by an expansion in volatility within a few days.

Interestingly, Wednesday was actually the narrowest range since the April 7 low

As well, Wednesday left a Lizard sell signal, a 10 day new high Topping Tail.

Downside follow thru today will trigger further sell signal, a Soup Nazi.

This is a new 20 day high that reverses back thru the prior high within a 20 day lookback the same day or the next day with at least 4 days separation from the prior high…to guard against ‘continuation’.

Of course Wednesday’s little reversal could be in the context of a pause following Tuesday’s breakout of a two week consolidation.

You know what Gann said, “two weeks on the side”. He was talking about distribution at tops or accumulation at bottoms.

The minor ‘reversal’ in the SPX accompanied Topping Tails in several vertical names:

LITE

NET

ORCL

ZS

In sum, markets closed mixed on Wednesday in front of a potentially decisive two-day stretch.

The DJIA slipped 92 points while the SPX remained flat. In contrast, the NAZ outperformed gaining 63 points.

Internals offered a mild bullish tilt: the NYSE saw just 18 net declines while the NAZ registered a robust 408 net advances

Wednesday’s significant development came from outside the tape.

The ADP Employment Report shocked markets, revealing that private-sector payrolls rose by just 37,000 in May—far below the 110,000 estimate and even April’s soft 62,000.

It marked the weakest reading since early 2022. It cast a shadow over Friday’s Nonfarm Payrolls report, raising fears of an economic downshift that could compel a delayed Fed pivot toward easing.

The question is whether Mr. Market in his typical perversity will take a weakening economy as a “bad news is good news” moment.

In other words, will bad news be seen as a catalyst for the Fed to cut rates sooner than anticipated, further underpinning the advance.

The rally is on the razors edge of the end of Gann’s Panic Window of 7 to 8 weeks.

Remember these panics can be Buying Climaxes or Selling Climaxes.

Continued strength next week would open the door to a continuation into early July which is 90 days/degrees from the April 7 low.

Once a panic goes beyond the 49 to 55 day Gann Window it usually stretches to 90 days/degrees.

This is in keeping with the two famous blow-offs in 1929 and 1987.

While there is a lot of chatter about a summer melt-up, leave it to Wall Street to extrapolate what has already been a vertical move.

While the indexes may not be at new highs, all you have to do is look at names like STX, RBLX, RBRK, AVGO, APP, WING and GEV to mention a few, to get a glimpse full frontal FOMO.

It’s not just tech. Frenzy has riddled the tape.

That said there are some chinks in the armor.

Sky Walkers like FRHC, NUTX, CRWD, and DAVE, to mention a few, have come in.

In sum, yesterday’s NR 7 Day comes a week ahead of the June 15th Jupiter/Saturn square discussed this week.

Of course these turning points are always + or – a week.

Consequently, what emerges out of this two week consolidation is going to be important confirmation of a continued uptrend or a change in trend.